Inflationship

How supply chain shocks impact consumer prices

Imagine canceling an Uber, but instead of just getting a new one in a few minutes, all the drivers vanish, the next ride costs 10x more, your new pickup spot is five blocks away, and surprise– in 3 months, now your $7 morning coffee costs $15 because of it.

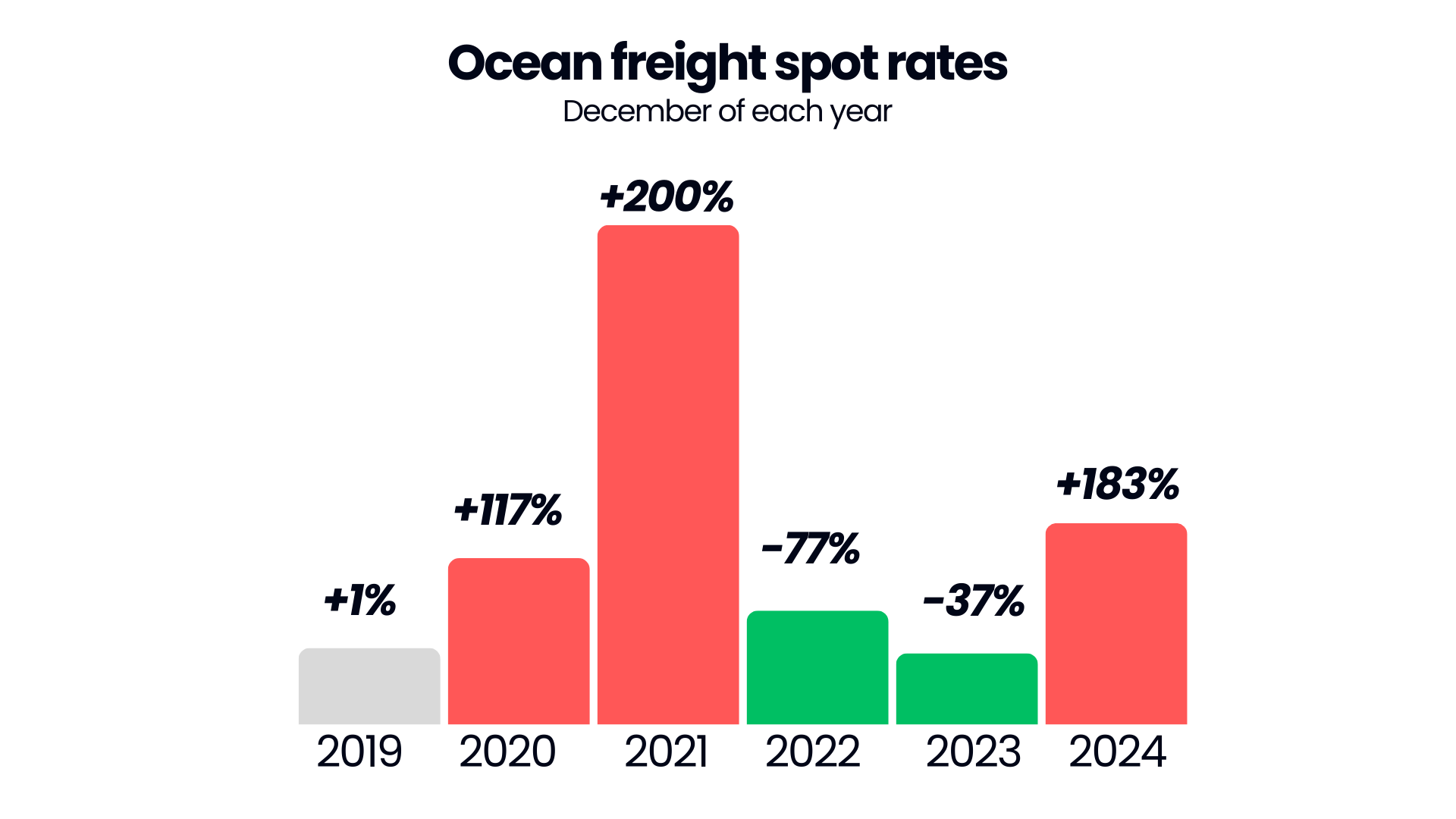

That’s what the ocean freight markets are like – and boy, are people “cancelling” their ships. In early April, ocean freight bookings to the US were down by 64% from the week prior as tariffs unfolded. Even now, May is expected to come in at least 20% lower in bookings year over year.

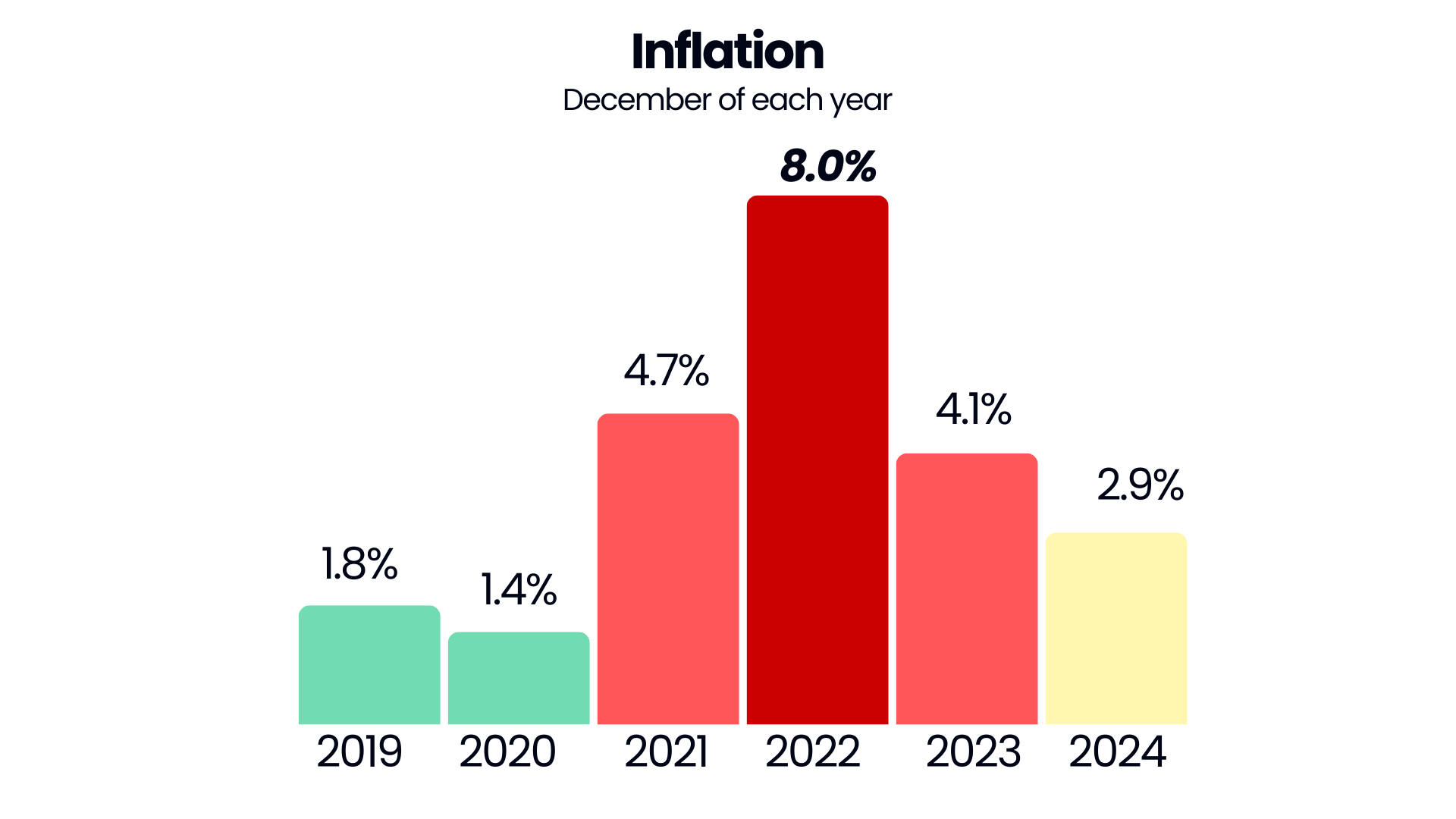

Last time this happened, we ended up with 10x freight container costs and 8% inflation two years later.

Inflation’s like that bad boyfriend that we can’t just seem to get away from. We know it’s bad for us, yet the drama of another shipping mess with China is too thrilling to let go of. And so we are here again – poking the supply chain right as we had a historic soft-landing, flirting with the prospect of higher inflation. In our inflationship (it’s inflation + situationship + it has to do with actual ships!).

So let’s dive in.

Big Ships

I’m scared of ships. Nothing would freak me out more than being in a giant ocean, surrounded by nothing, on a giant floating container with no way off. For a month! It sounds terrifying.

Yet 16 million giant, brave, cool freight ships move our stuff each month – 1M of those are from China to the United States. Each ship carries ten thousand containers, each one worth $1.5K just for a one way trip.

And in September 2020, those ships got stuck.

Billions of dollars of goods would have to wait up to 4 weeks in line, on the sea, to be able to enter the ports of LA and NY through 2021 and 2022. Just floating there. Stuck on a ship, with the crew probably running out of food, not being able to land.

Ports got jammed as there were too many ships for the amount of docks, cranes and yard labor available. They simply didn’t have a stop button as America kept pressing Add to Cart for its goods and overloading the entire global supply chain with each click.

Stuck ships

Part of the bottleneck was driven by increased demand. The Fed slashed interest rates, bought back bonds, lowered loan expenses, and made us all feel richer and more likely to spend on 3 different House of CB dresses and its 5 Amazon dupes. Congress sent checks and unemployment bonuses to people, further boosting spending. Bridgewater shows HERE how household spending has been driven up by government stimulus over that time.

And the nature of the demand changed— e-commerce boomed. 2021 saw tons of new online store openings as entrepreneurship went mainstream. Shopify alone added 600K new stores between the end of 2019 and 2021– with 2020 bringing its largest gains in net new merchants added.

Fueled by our post COVID shopping addictions and open wallets, retailers rushed to get in stock. Inventories grew significantly for two years through 2022 – in a much more volatile way than the usual 2-3% annual inventory growth rate.

Cancelled ships

Yet our plumbing to support this growth was super outdated, and full of traps.

In the few weeks of March 2020, when demand froze, ocean carriers had to suddenly cancel – “blank sail"– a huge number of ship bookings to buffer collapsing demand. When ports reopened, they did so unevenly, demand patterns changed, and therefore all the routes were different. All the ships were in the wrong place.

Factories in China were packing up goods meant for ships that were still stuck in the US and more empty ships were going from US to China. It’s expensive and inefficient to try to reroute all these ships (quick math means one ship voyage is worth $10-20M in shipping revenue)– so carriers just drove up cancellations to reset schedules.

All the new Shopify and e-commerce stores added extra complexity – instead of moving one full container for someone like Walmart or Costco or Tesla, shippers were coordinating thousands of less than containers (LCLs) to make up full containers, and then coordinating different less than truckloads (LTLs) to make full truckloads across different hubs to different destinations.

It is amazing that shipments even got to their destination at all. But they did, for a much, much higher price.

By July 2021, container costs went from $1K to $10K – a 10x increase, where they stayed for nearly a year. It’s kind of like surge, but with the global economy.

Rich ships

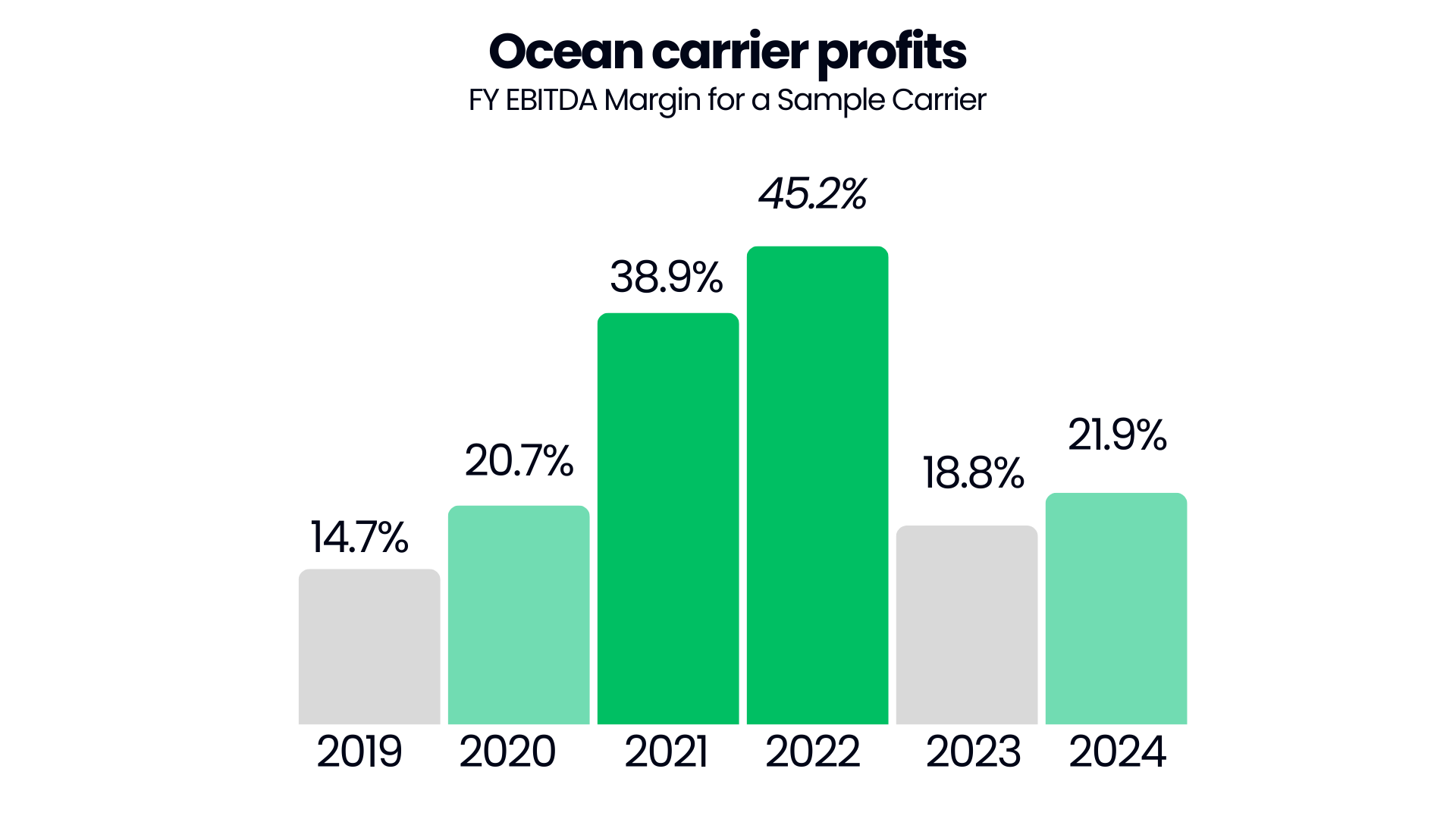

In 2021, Maersk, an ocean carrier, the second most bravest and biggest shipper of ships, nearly doubled their revenues and tripled their profits year over year. They made more profit in 2021 than they had for the 3 years before that combined!

Carriers all over increased their contracted freight for better reliability, upsold customers on new routing and logistics services, and upsold more reliable services to their highest paying customers for higher rates.

Inflation Ships

Take the extra shipping cost, add the cost of overstocking to support the 2-4 week delay, add the higher truckload cost (which saw a similar dynamic as ships though not as intense), pass the cost on to the consumer from the retailer and there you have it – an 8% increase in prices by 2022 that shook the nation to its core and probably altered the future of America another two years later.

And that’s how bottlenecks and shake ups cause rapid supply and demand volatility, impacting pricing in every step of the chain. It’s why pausing shipments, altering supply chains, and adding extra instability, especially in our slow and outdated, low visibility supply chain is risky business.

Today’s Ships

So here we are, 5 years later from the pause that started it all – back at it again (Alex Cooper voice).

We already know containers have been paused in April 2025. The impact is still to be felt. It takes 30-60 days from containers to make it from China to New York and LA; we have a week or so until we start feeling the first effects. Retailers are bulked up – inventories for even Jan and Feb were at peak levels in prep for tariffs — but sales year to date have been strong as well.

What we don’t know is how long these trade shocks will continue and how strong consumer spending and inventory demand are going to be. Big retailers and carriers are acting fast to move in light of volatility, either way. According to the Flexport CEO, volumes are now being rerouted to India and Vietnam. More volatility means more room for error, more room for new lanes, more empty ships, more blank sailings, more delays down the line if the world can’t stabilize in time.

If demand remains strong, this could mean tightening and more profits for carriers like Maersk down the line. Their stock price is usually correlated with the Container Spot rate and this rate has been dropping so far this year per the impacts above. The calm before the bottleneck.

The key things to look out for are going to be signs of weakening demand and walk back from trade war; a calm recovery is now at stake.

Potential scenarios going forward in 2025

But there’s a bigger picture as well.

We think of the supply chain as some mysterious, behind the scenes, after thought — yet it drives everything in our life. When it gets triggered, it cascades into second and third order consequences in a chain that is consistently forgotten and underestimated.

And if inflation is all about the certain, efficient flow of goods — it rises as stuff gets stuck (in transport, or labor, or bureaucracy) — this whole decade of volatile inflation is a symptom of our society’s obsession with hype and bits while glossing over fundamentals and atoms. The real things.

The global economy just got very interesting again.